There is this hockey-stick moment at the beginning of almost every retail media business that sees astronomical growth for seemingly very little effort. Retailers see an influx of dollars with year-over-year growth at 30–40%, and revenue-per-head in the $3–4M range (typically not accounting for a third support that complements that growth).

On a base of $10M or $20M, an extra $5M in net-new revenue per year looks astronomical. If we can just maintain this level of growth, we'll be a billion-dollar retail media business in no time!

But zoom out. We're living in Amazon's world, baby.

This is not to dissuade you — quite the opposite. I want this to fire you up. And I want you to send this, and another article (Retail Media is a Competitive Moat), to your CFO and CEO with the subject line: "We need to get moving." There is so much untapped potential out there just looking for a viable alternative.

What your leadership needs to know is that Walmart and Amazon didn't get there by their dominance in the market (I was there, I promise you this). Walmart's leverage was not the catalyst for its rapid acceleration in retail media — and Amazon is proof of that. Amazon was 1/3rd the size of Walmart in 2017 when it surpassed $5BN in retail media revenue — approximately where Walmart is today.

This is not free money. And if you're treating it like that, know that your advertisers (suppliers) can smell it from a mile away.

Part No. 01The opportunity.

Before I lose you, I want to bring us to the benefits for retailers with scaled retail media businesses:

- A mutually beneficial flywheel between their suppliers and themselves.

- Significant growth in operating income.

- Protection against competitive threats.

- Increased engagement with customers.

- …the list goes on.

The reality today is that retailers are investing around 0% of capex and less than 0.1% of opex on this opportunity — because it looks easy at the start. And if you're doing that, you're likely growing with or below the market, meaning your competitors are getting stronger, smarter, and more efficient while you make small incremental gains.

Part No. 02The symptoms of initial growth.

In the beginning there was trade marketing… then shopper… then retail media. Over the last 10+ years we've experienced a migration from shopper marketing (resource-intensive, heavy in-store) to retail media (digital). This migration has taken place at different times across the retail landscape, contingent on retailers establishing a greater digital presence — many are still going through it today. (Retail media is now working its way back into shopper marketing — but that's a different topic.)

What's consistent about the 'shopper marketing' budget across all of retail is that a lot of those budgets are spent outside a retailer's purview, via third-party execution partners. Retailers have limited visibility into how their suppliers invest dollars to support mutual growth.

As dollars migrate into retail media, for the first time the retailer gets visibility into those dollars — which to them look net-new. In this phase, a retail media business might grow 30–40% year-over-year, and do so in an incredibly efficient way (reasonably little effort). Why?

Part No. 03The Great Stall.

Inevitably, every retail media business hits a stall — a point where growth drops to approximately 0–15% (less than market). Walmart hit a stall in 2016, which precipitated a complete rethink of the model.

The Great Stall happens after most or all of the applicable dollars already in the retailer's orbit have been absorbed into retail media. To this point, it's been easy — you're really only competing against yourself.

This effort is surprisingly less complicated than you think — and it's the reason I write this newsletter every week.

Part No. 04The cost of breaking the stall.

Last week I talked about three baseline ways a retailer can establish a competitive moat in their retail media business:

- Make it easy and appealing for advertisers to buy.

- Make it easy for the retailer to operate.

- Make it competitive.

Combined, these are what ultimately drive growth. If you make it hard to buy, they won't work with you. If it's too expensive to operate, you can't scale.

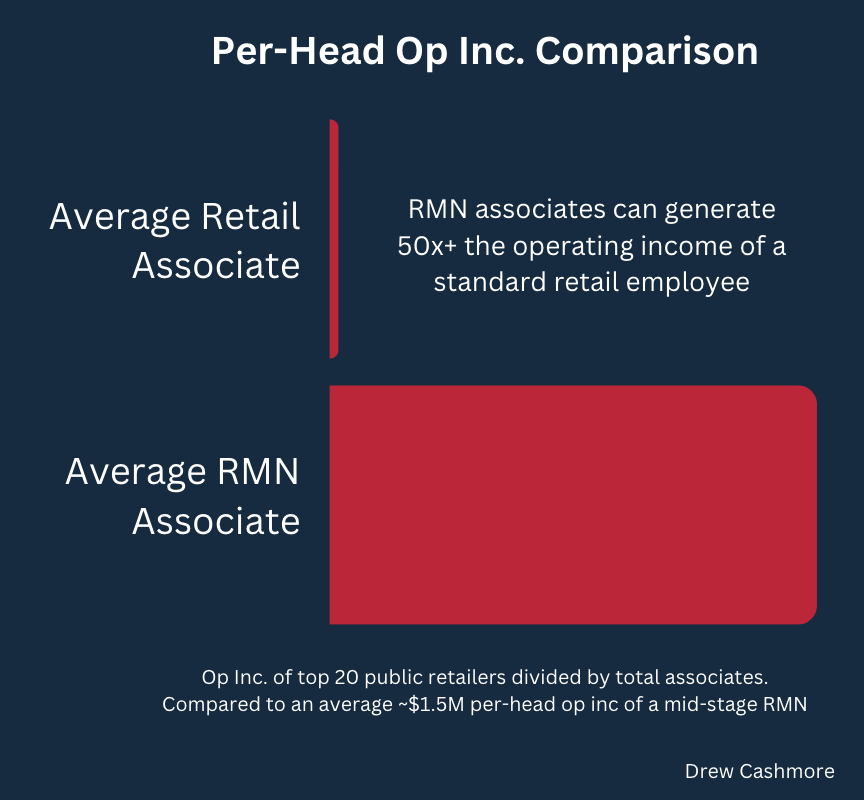

In the olden days, I would have told you to throw people at the problem. Imagine taking your revenue per head from $3M to $750k. Imagine taking your net revenue from 83% to 56%. Imagine hiring hundreds of new, specialized resources in media markets around the country — plus the new infrastructure, incentive models, and cultural shifts to support it. If you were to in-source the business in its entirety (tech and resources), that's roughly what it would take. The good news is that's not necessary anymore — but it's not that far off. I broadly summarize the stages that help a retail media business accelerate as:

- Unification of technology — a single operating, planning, buying, and measurement tool to simplify activation.

- Enhance the go-to-market — make it optically more appealing; invest in B2B marketing and your sales team.

- Change management within your organization.

What's great is we've moved from the need to build in-house, to incredible support engines for both technology and services. But these cost money. The future mix of a path to acceleration looks something like 60–65% net revenue and ~$1.5M per head.

Don't fret — when you look at the operating income generated by a retail media employee, the benefits are clear to any retailer's overall bottom line.

But the caveat is it can't just be growth off a dilution of margin in the retail media business itself. Medium risk, stupidly high reward (to be dramatic). If you want to make money, you need to invest to do so.

Part No. 05The risky, failing alternative.

Retail media doesn't grow on trees. But what we're seeing are some vendors promising significant incremental revenue for low-to-no cost or effort. Be wary of the snake-oil salesperson in retail media — what seems too good to be true almost always is.

- What looks like a paltry 5–10% of revenues in exchange for 'incremental money' looks more like 20–30% when you stack in hidden fees.

- What you believe is best-in-class technology has a lot of cut corners — because if nobody is paying for the technology, nobody is investing in it.

- What looks like passing advertisers to a partner to activate on your behalf is actually you losing more and more control of your most important relationships — your suppliers.

This is not to say "don't work with partners" — in fact, the exact opposite. But find the right partners that are:

- Incentivized by your growth, not the growth of everybody else.

- Ingrained in your business, and intimately understand and respect it.

- Willing to help your team learn, grow, and absorb over time.

- Transparently charging for their service or technology — if it's free or the cheapest option, know they won't be willing to invest in your business.

Like almost any great business, growth comes from a willingness to take risks and invest — in people, technology, and promotion. The market continues to consolidate at the top today because there simply aren't enough competitive offerings. But know that if you take that leap and invest, there is so much growth still ahead.

If this resonated, share it, comment, push back. And subscribe to the Retail Media Leapfrog Series for more.