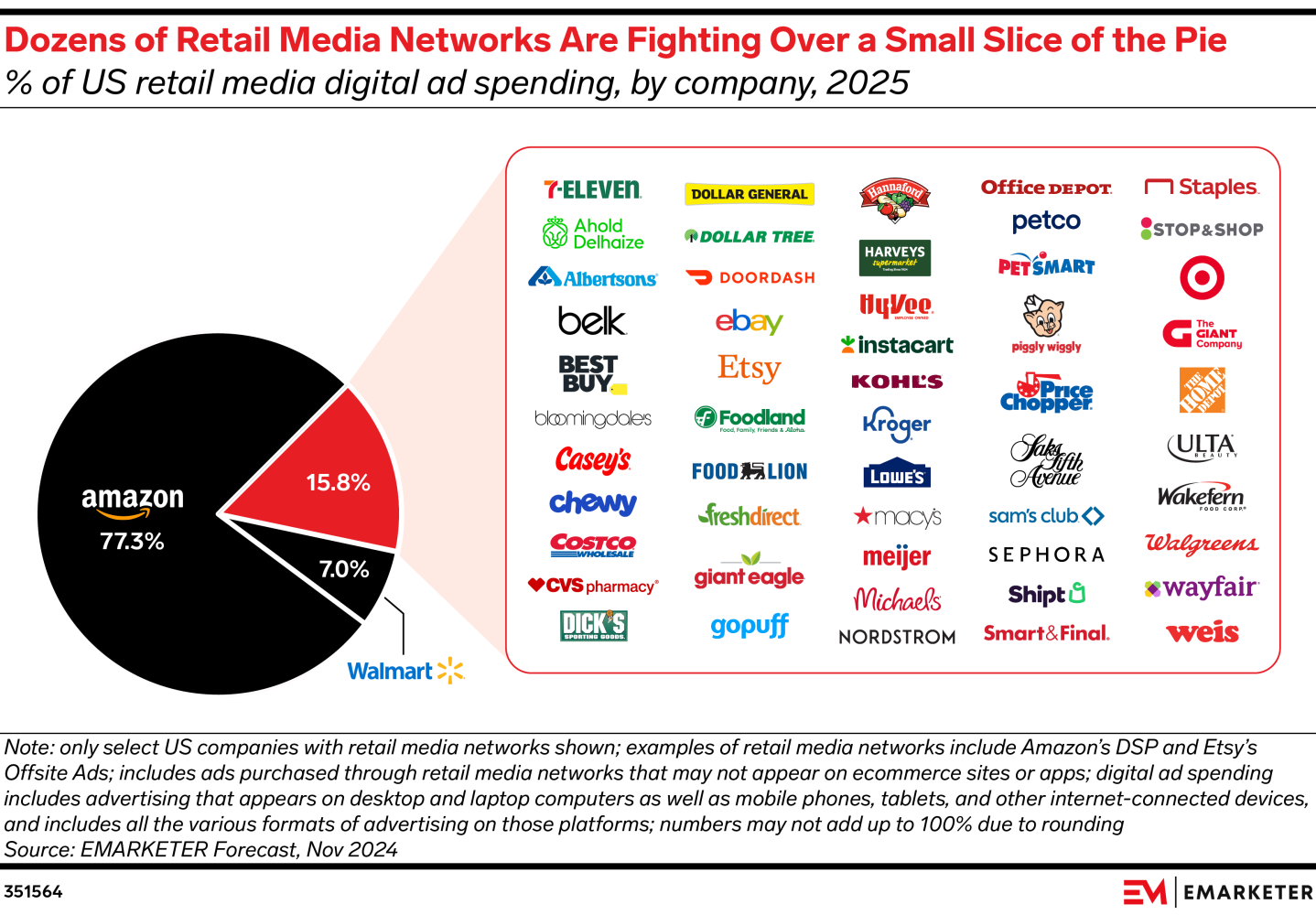

This week, eMarketer released a revised growth trajectory for retail media that projects a slowing pace of growth for the industry overall — as well as a slower pace than historicals for Amazon Ads (which makes sense; it's already at a $69 billion ARR).

Over the next four years, the retail media industry will grow 88% to a $98 billion TAM by 2028 — so it's still an incredibly important area of focus for the media, advertising, and retail industries.

But what fascinated me was the projected percentage of the pie that Amazon maintains through 2028. Hint: it doesn't change. So while retail media will see an influx of $46 billion over the next four years, Amazon will always own approximately 77% of the pie — and that's a serious problem for almost every other retailer.

What Amazon can do with these monies — invest in innovation, drive more traffic, reduce the cost of goods for customers, improve experiences, reduce operating costs, grow sales — dwarfs that of any other retailer. It has a compounding effect over time. A flywheel, if you will.

And it doesn't just impact ad investments — it impacts trade investments as well, because continued growth creates a better negotiating lever for Amazon. A lack of serious, competitive participation in retail media from other retailers simply fuels this flywheel, shifting more and more supplier trade and advertising budgets to the behemoth.

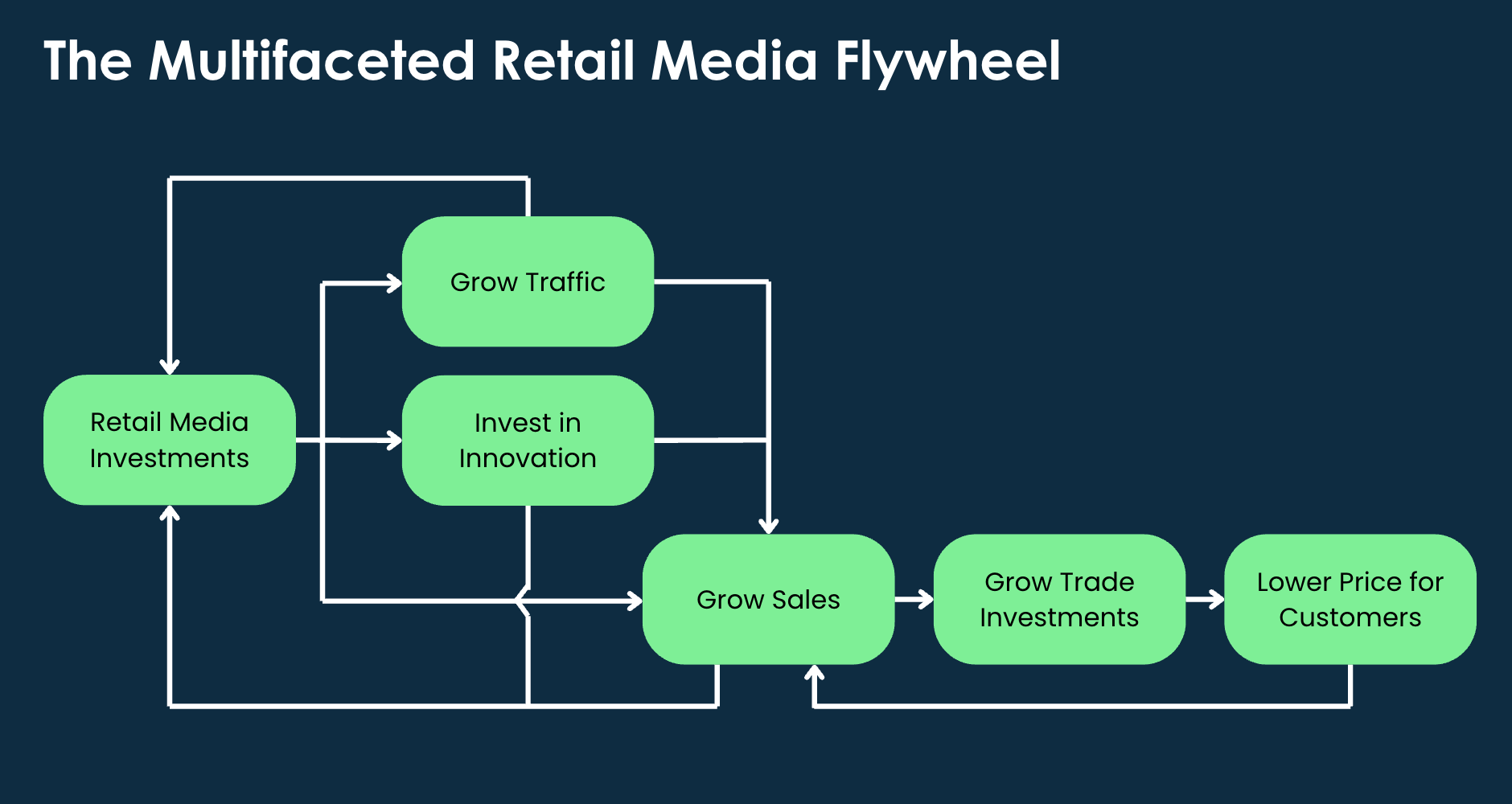

Part No. 01The [multifaceted] retail media flywheel.

There are a bunch of different versions of the retail media flywheel, but mine is by far the most unnecessarily complicated (it's how I roll).

Retail media, to me, has always been ingrained as a core tenet of the overall retail proposition (as were shopper and trade marketing before it) — suppliers co-funding the growth of the places they sell. If your flywheel starts with 'retail media investments,' those investments can have substantial benefits for a retailer's overall business:

- Working media drives traffic — online and offline.

- Working media drives sales — online and offline.

- Higher-margin ad spaces create operating income that can be reinvested in things like innovation.

But more importantly, growth in the business creates increased perceived value of an individual retailer — and improves that retailer's ability to negotiate on trade investments.

More trade investment lets a retailer reduce costs for the customer, which generates more sales and further perpetuates the flywheel. Amazon knows this — and it's why they have a disproportionate share of overall trade and retail media investments.

Part No. 02The opposite of growth.

The opposite is also true — but not in an obvious way for most retailers yet. If the flywheel is perpetuating itself at another retailer (in this case, mostly Amazon), then Amazon can continue to significantly outpace the market in overall growth.

We see this in earnings reports across the industry, with many retailers seeing declining sales in spite of growth in overall retail sales (however slight), and growth in Amazon's retail business. Yes, there are myriad factors — but I argue that the retail media flywheel Amazon has built for itself (its own competitive moat) is having a far more significant impact on other retailers' declining sales than they can quantify today.

It's not just Amazon — several other retailers have established strong foundations that let them compete: Orange Apron Media by The Home Depot, Walmart Connect, Sam's Club Member Access Platform (MAP), CVS Media Exchange (CMX), and Best Buy Ads, plus well-established European RMNs like Asda and Morrisons.

A lack of growth relative to the market — or worse, declining sales — has the compounding effect of limiting or reducing trade and retail media investments. Those dollars ultimately end up in the hands of retailers that have competitive offerings. What many retailers still perceive as internal competition for trade vs. shopper or retail media dollars is false: your real competition is with retailers that have scaled retail media offerings.

And with trade investments alone representing an estimated 30–50% of the overall operating income of many major grocery and big-box retailers today, declining investments can have a detrimental impact on these retailers' ability to operate in the future.

Part No. 03Creating a competitive moat with retail media.

There's a lot more to this than a single post can cover, but I propose three baseline ways a retailer can establish a competitive moat in their retail media business. These are really important to do together:

- Make it easy and appealing for advertisers to buy: unified buying platform, buy how you want (self-serve direct, managed service, 3rd-party bidder), second-price auction, quality measurement.

- Make it easy for the retailer to operate: a retail media operating system in one tool, workflow automation, fewer tools, media supply-chain efficiencies.

- Make it competitive: pricing, tactical proposition, differentiation, B2B marketing, measurable outcomes.

Done together, these baselines allow for differentiation that can drive net-new dollars into most retailers' retail media businesses. But getting there requires a leap of faith at an executive level. For that, we need to look at:

- Real investment in the business — not as a small percentage of retail media revenues, but as a significant strategic investment from the retailer P&L overall, to support technology, resources, and marketing.

- Coordinated go-to-market between merchandising and retail media, so trade, retail media, COGS, and retail sales are looked at holistically.

- Specialized talent and executive leadership that establishes retail media as a core tenet of the overall retail strategy — not a side project.

- Strategic effort to find the right technologies, tools, partners, and business models that let individual retailers own the key relationships with their advertising partners (their suppliers) and drive mutually beneficial growth over time.

Still hope — but not a lot of time.

Even in a nascent state, retailers still have the space to create competitive moats out of their retail media businesses. But they don't have a lot of time to do it — the horizon for viable participation in this space at scale dwindles with every quarter.

If this resonated, share it, comment, push back. And subscribe to the Retail Media Leapfrog Series for more.