First — the Retail Leapfrog Series is back by semi-popular demand, but this time in the form of a newsletter. It turns out I have a lot more to say that nobody else is talking about. On Sunday mornings I'll be pouring my thoughts into helping new-and-emerging retailers leapfrog competitors in the retail media game by learning from the mistakes and thought processes we had at Walmart and other retailers over a 15+ year period (before it even had a name).

The target for this newsletter is not retail media people — although it'll certainly help frame things with your partners. Rather, this is for you merchants, retail marketers, and operators — because you are the lifeblood of retail. Share with your friends.

Today we're going to talk about retail trade spends, their apparent fungibility with other supplier spends, and the risks in that to retailers. I saw some real data on this topic, and I think I may have had at least part of this equation wrong.

If you haven't read it, I wrote about Trade vs. Shopper vs. Brand dollars against an underlying assumption that these dollars are all fungible and therefore retailers can dictate the terms. Specifically: that all three types of funding are important to the symbiotic retailer–supplier relationship, and that you as a retailer are not entitled to all of that money unless you have the right mechanisms to support it — because today these dollars are intentionally assigned to specific activations.

Part No. 01Dear merchant friends, you were right.

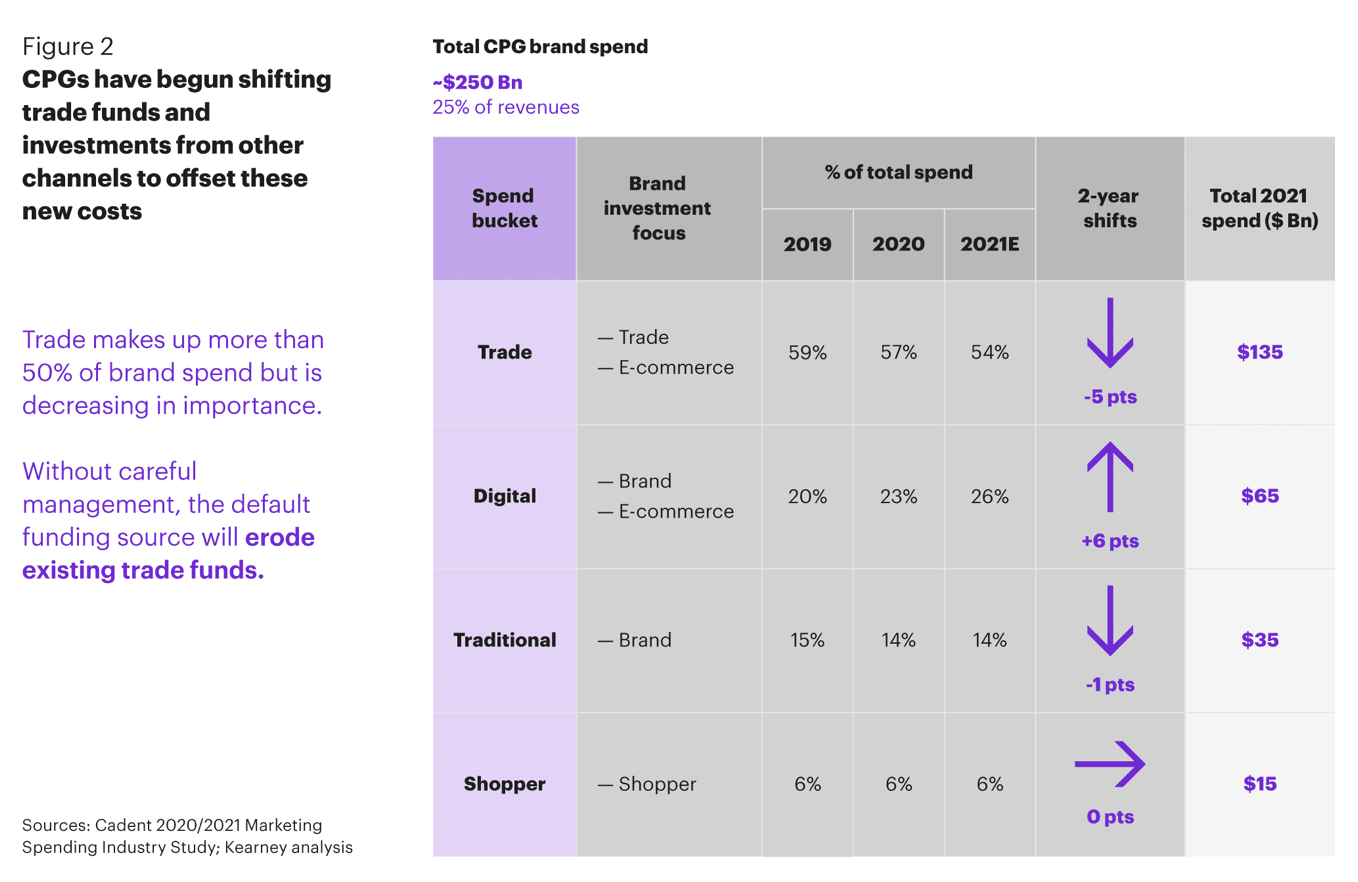

This post isn't about the distinction in budgets per se, but rather the fact that those budgets are actually shifting — at least according to a 2021 Kearney study on retail media by Katherine Black and Nora Kleinewillinghöfer.

I'm sure there's more updated data out there, but this chart (reposted and summarized recently by Don Brett) most perfectly encapsulates the shift. I can only assume it's become greater as we scale out retail media. Worth noting: the total dollars remain flat, but how CPG brands invest is changing at a macro level.

Part No. 02If it's one big bucket, keep it in trade… right?

As a merchant, this makes sense to me — if I can keep the dollars in trade, it goes into things I control. It lets me offer great prices to my customers, supports the things I want to focus on to get my comps, pads my P&L (which I'm incentivized on), and the way I spend those monies has historically worked.

But from a brand perspective, I'm not so sure. As a brand, can I truly get quantifiable value from my trade investments? Some retailers charge slotting fees, some charge for eCommerce fulfillment, some charge for innovation or access to merchandising tools or flyer inclusion. I'm often blind to the outcomes — not in control of those spends — and I sometimes see those dollars going to grow my competitors' brands.

Part No. 03Is the shift a good thing?

I was initially inclined to say yes — because it rebalances the equilibrium between retailer and brand and forces both to focus on what's right for their connected but mutually distinct organizations. But when you go back to the original purpose of trade, it was a 'tide raises all boats' proposition — and more importantly, it often served to reduce costs for the customer. In that, it's incredibly important that trade maintains its dominance in the retailer–supplier relationship.

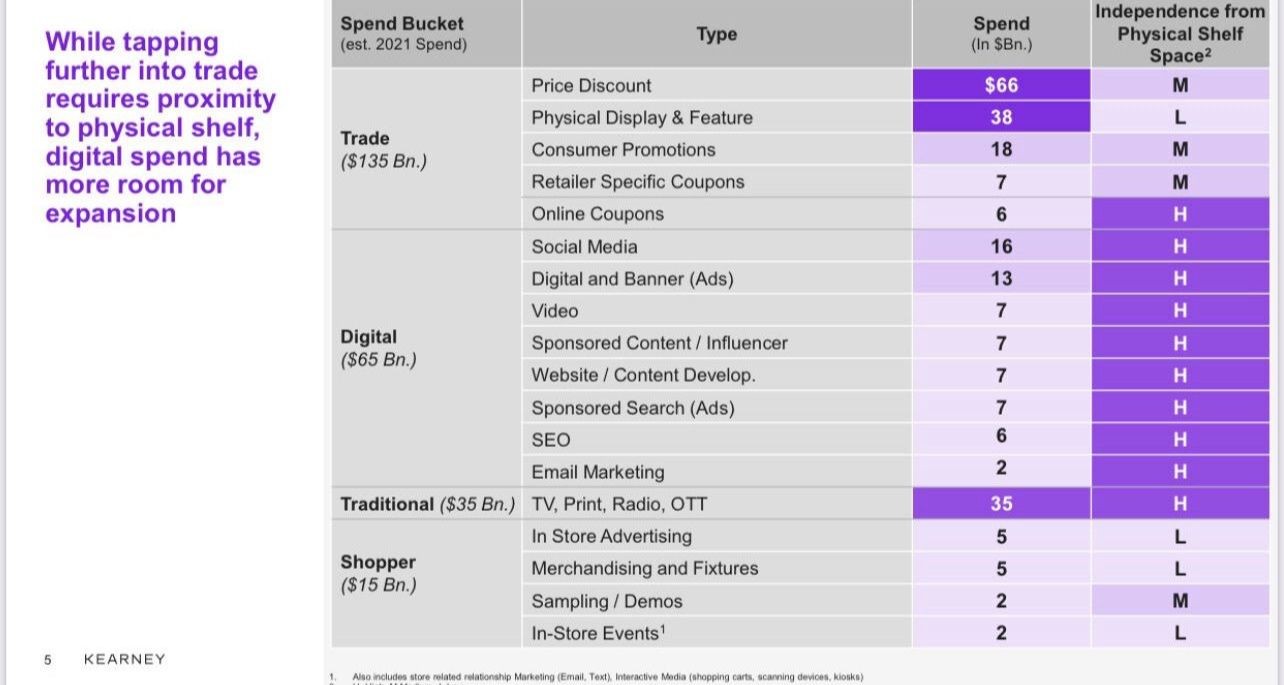

As an extension of that point, it's worth highlighting one other slide in the Kearney report:

First, this slide clearly articulates the distinction in funds — suggesting they are in fact different. It also highlights the 'independence,' or proximity, certain promotional vehicles have to the physical shelf. (I'd argue the distinction between a digital and physical shelf is unnecessary, so for buckets like 'Sponsored Search' we should put an L beside it — search ads are close to the shelf.)

What this makes me realize is how much of the 'new' in retail media is beginning to move away from the shelf — CTV, offsite media, DOOH. Sure, it might be powered by shopper data, but it's distinctly separate from reaching a customer in a shopping mindset.

Back in 2009 when I first started at Walmart, I used to say: "brands spend all this money promoting themselves on TV and radio and social, but when it comes to the shelf, they divorce themselves from the conversation." You invest all your marketing in non-shopping vehicles, and when a shopper reaches the #FMOT, you're nowhere to be found.

Part No. 04Before everyone gets mad at me.

We're not there yet — not even close. In my [expert opinion], any given retailer's 'fair share' of retail media investments should sit in the realm of 1% of gross revenue. At that stage it's mostly a shift in 'shopper,' not a true 'incremental' investment — so you should not see any movement in trade investments, and if you do, you should push back.

Past 1%, you have to reach a level of sophistication where you can tap into truly 'incremental' budgets (the 'brand' budgets) and compete with the likes of Google. What's important in all of this:

- Getting to 'fair share' is no longer achievable without sophistication in retail media — you have to invest and work at it now, because the competition is so great.

- While the budgets seem fungible, the spends are still mostly allocated by bucket. If you don't have solutions to support those buckets, you won't capture those monies — and they'll inevitably go to grow your competitors.

Most importantly, much of the need for a shift from trade to retail media is coming from the massive dollars flowing into Amazon ($45BN in their retail media business today). It's entirely possible that if you're seeing a degradation in trade investments, it's because brands are spending so much on Amazon that they're forced to limit spending elsewhere to do so.

Closing thoughts.

It appears there is in fact some fungibility between buckets of funding on the supplier side — but as a retailer, it's not enough to try to capture it solely in one bucket. You need to be offering retail media and shopper marketing solutions if you want to capture funds in those buckets. If you don't, those dollars will absolutely go to fund your competitors' businesses.

If this resonated, share it with a merchant friend, comment, push back. And subscribe to the Retail Media Leapfrog Series for more.