Remember why we are all here… because millions of people shop every day. When I started my retail media journey at Walmart in Canada in 2009, we looked to Europe as a guide for what to build — how to better operationalize in-store, how to architect for omni-channel, how to think about loyalty or online grocery.

Over a decade-and-a-half later, Europe still has a differentiated approach to retail media — they built this thing for and with the shopper in mind. It's a refreshing approach that we need to consider across the rest of the world.

But over the past year, I've seen a convergence of narratives and strategies around retail media on a global scale. Instead of learning from the uniqueness of each market, we seem to be focused on replicating just one approach.

In this week's Retail Media Leapfrog Series — a collection of thoughts designed to help retailers leapfrog incumbents by learning from others — I'm publishing a talk I did at the recent IAB Europe Retail Media Summit in Amsterdam about the lessons we can all take from the European retail media market.

Part No. 01A retail media crystal ball.

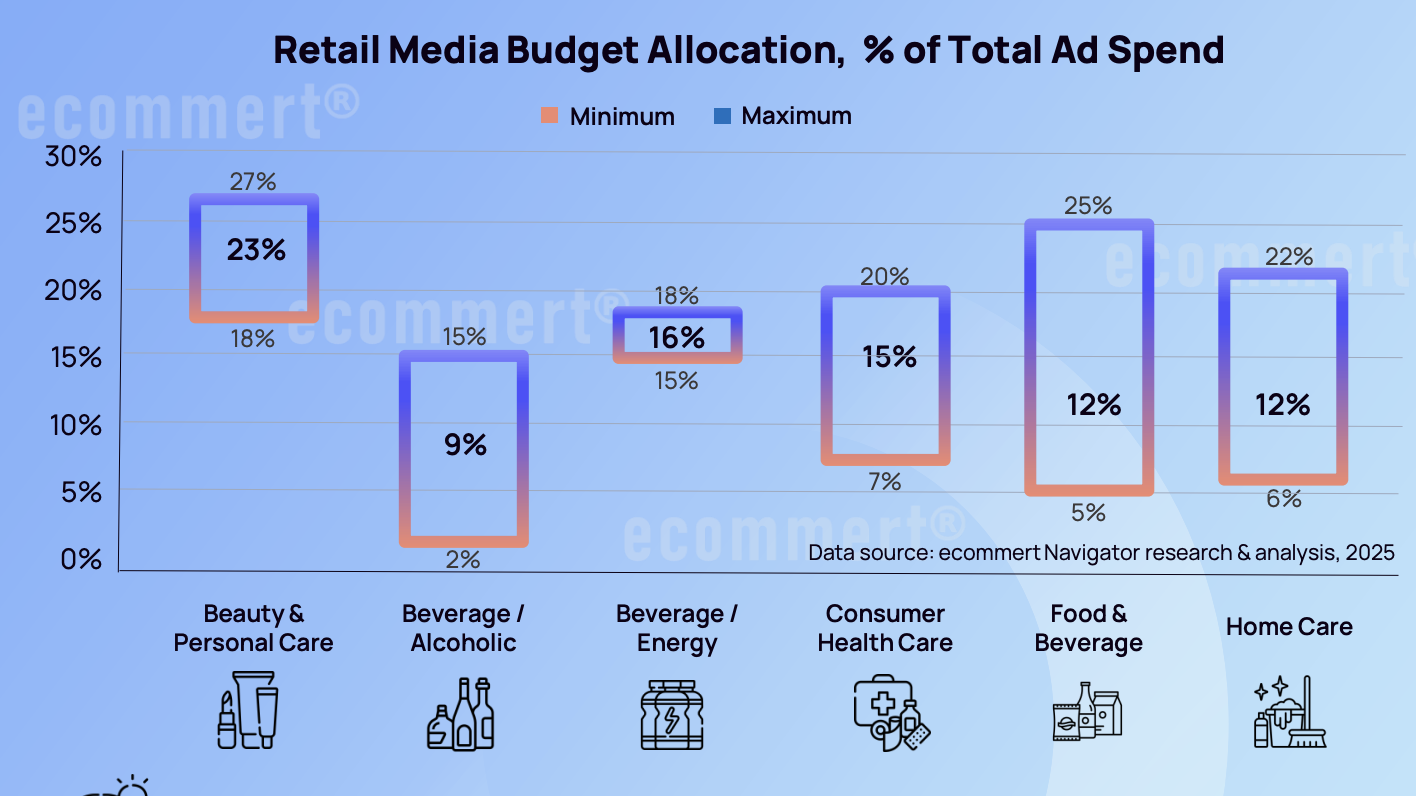

A 2025 study by ecommert has retail media in the U.S. sitting at 17.9% of total media spends (Sarah Marzano and Bill Fisher might have a clearer view on the actuals here). That's compared to its European projections of 6%–18% across categories. Ecommert considers the European market "established, but still evolving best practices."

If the U.S. is slightly ahead in maturity (or at least adoption), it can give us a crystal-ball view into what might happen in the European markets if they follow a similar path.

And what we're seeing in the U.S. market is an incredibly powerful media offering — one that we should be proud of — but with extreme consolidation at the top.

Because the U.S. market prioritized digital as the core tactic in retail media (specifically sponsored product ads), it meant that every retail media business inadvertently positioned themselves as a direct competitor to Amazon and Walmart — who are really good at sponsored product ads.

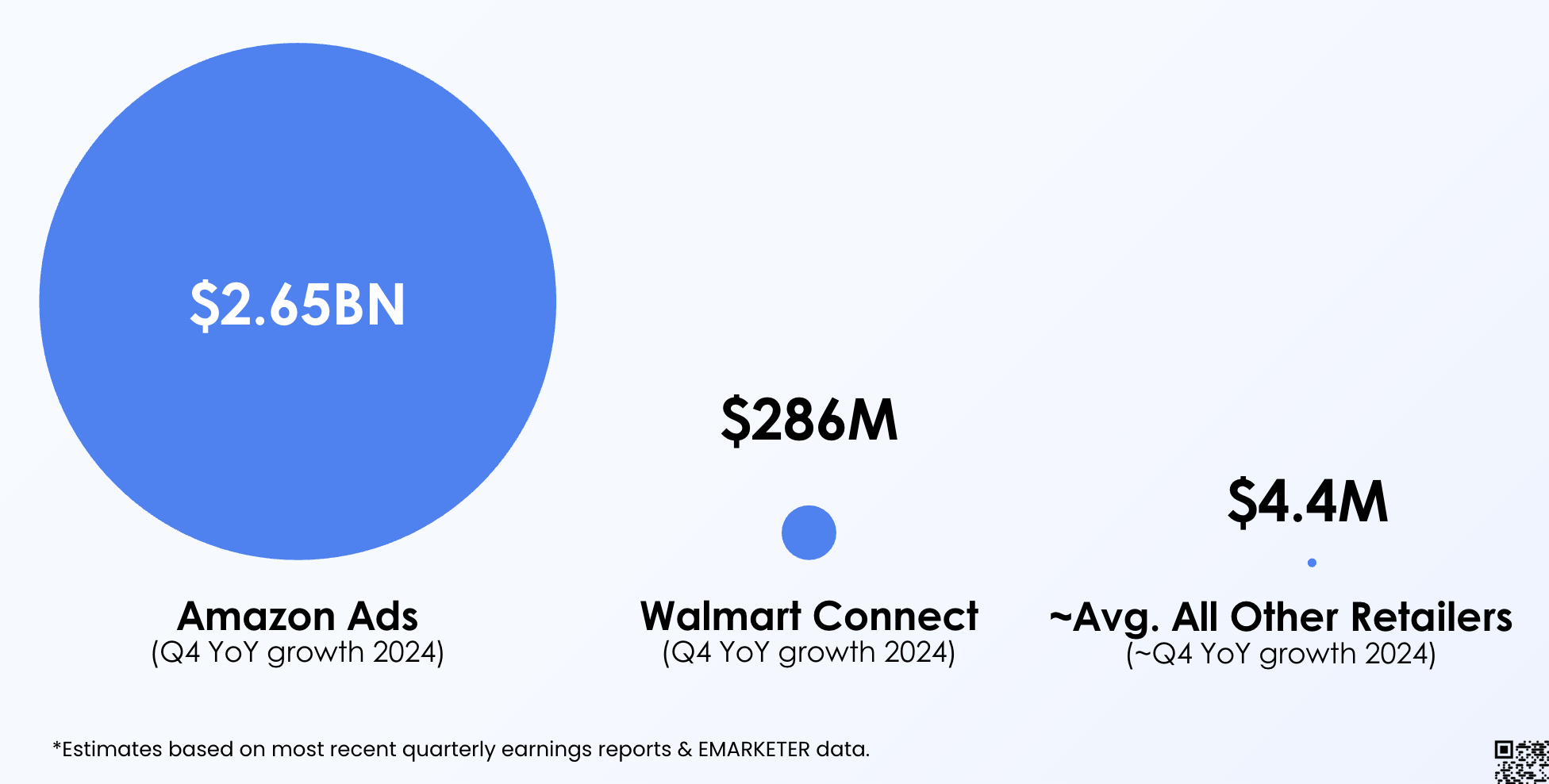

What that actually looks like is Amazon adding about $2.5BN in top-line retail media revenue every quarter — more than the annual growth of the rest-of-market combined, every quarter. The compounding effect spins their flywheel, and allows those retailers to grow their overall business disproportionately to others in the market — funded by advertising budgets.

As Colin Lewis discusses in his new Amazon flywheel, "Amazon no longer wants to own shopping, they want to own advertising" — because it's the perfect growth engine.

With growth compounding at the top and Amazon and Walmart moving further away from the pack, you start to see some concerning things in the data. Said differently: rest-of-market in U.S. retail media appears to be hitting a stall.

I argue the reason for this is, in large part, because of:

- An overweighted focus on sponsored product ads.

- Businesses built in a silo as pure profit centers, with expectations of high growth rates for little effort.

- Slower maturing of tech architecture and op model because businesses often lack strategic investment.

The market is maturing and starting to take retail media seriously, but the gravitational pull at the top is incredibly strong.

Part No. 02The standard path to retail media.

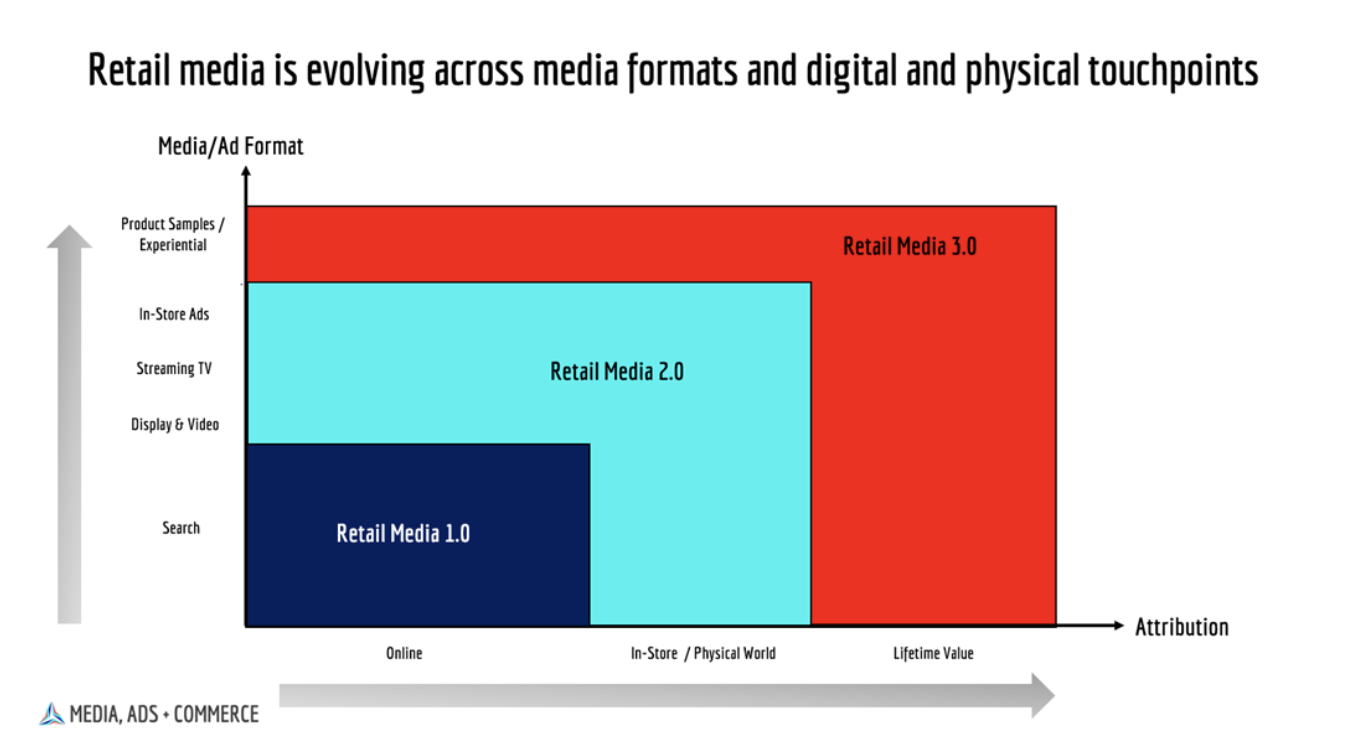

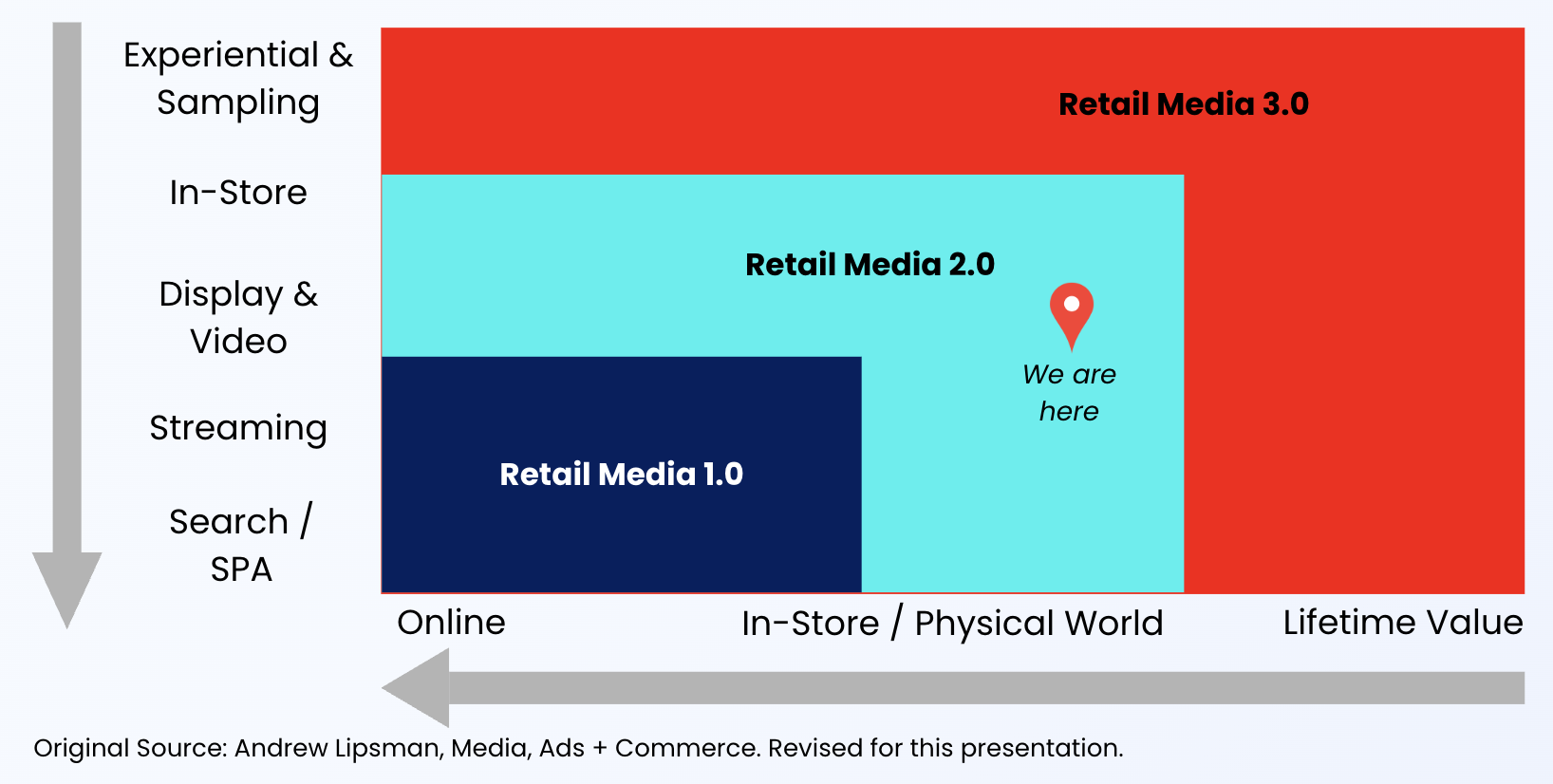

Andrew Lipsman clearly articulates the maturing of retail media in the U.S. — from sponsored product ads all the way to in-store experiential. And according to Daniel Knapp, Chief Economist for IAB Europe, we are in the Retail Media 2.0 era.

The overall opportunity grows as we expand outward, with in-store obviously being the holy grail of scale today. This path to growth has been repeated reasonably consistently across retailers — partially because the same people are often driving the strategy, and partially because retailers are mimicking the top of the market. Today this manifests as:

- More inventory — CTV, in-store, influencer, and so on.

- More sellers — 'demand' partners, programmatic onsite, passing audiences or inventory to 3rd parties to sell on the retailer's behalf.

Walmart took this path — they started with sponsored product ads (or search), because they were watching the meteoric rise of Amazon Ads leveraging the same tactic.

Yet purely mimicking the path of a Walmart or Amazon lacks nuance. Getting to a scalable, competitive offering required significant investment in technology, resources, and strong change management within the organization — as well as the advertiser community.

It also required a strong initial foundation. That foundation came from a migration of 'shopper marketing' dollars into retail media. In the early days, Walmart had an established shopper marketing business. Yet it convinced their suppliers to do less sampling, less experiential, less in-store signage, and convert it all to search because "that's where you're going to get the best and most measurable ROI."

Europe didn't do that.

Part No. 03Europe scaled the most difficult part first.

Building a scaled operating model for in-store retail media is one of the toughest things that other markets struggle with today. The transition to physical; the willingness to invest in digital screens; the ability to operationalize physical assets at scale; the desire to do so even when the margins are less than owned-and-operated digital ads.

But it's a necessity to create a differentiated, competitive offering against those retailers that are really good at the other thing (sponsored product ads).

I agree with Daniel — we are in our Retail Media 2.0 era. But Europe is running the playbook in reverse order: sticking to what retailers are good at, and expanding out to more unnatural media types and technologies.

The infrastructure to support in-store and experiential already exists within the ecosystem that surrounds most retailers across the globe — it's just often entirely outsourced. What Europe did was wrap a new commercial and operating model around a legacy approach, to create a scalable solution to in-store. Europe has taught us that in-store:

- Can scale.

- Can be highly profitable — for both the retailer and the advertiser.

- Can be measurable.

- Doesn't have to be scary or expensive.

That's what I saw from my early days of understanding this market to now. On the surface it would be simple enough to stop there. Congratulations, Europe — you have a working model for in-store retail media.

But to me, Europe's core differentiator, their secret sauce, is their relentless focus on what actually matters.

Part No. 04What Europe can teach the rest of the world.

The dichotomy of focus and philosophy is built right into our B2B retail media websites. Remember who we're building this for.

European retailers have built a truly customer-centric retail media ecosystem. Not as a sales strategy or talking point, but as a core philosophy driving this market forward.

Yes, we sell ads. Yes, we need to make money. Yes, we want it to be incremental. But when we focus on the customer — and our advertiser's reasonable needs over our own — we create sustainable growth propositions that are truly differentiated. To me, there are four philosophies to learn from in the European market.

01 — Retail media is omni-channel by default.

A digital-only proposition puts us squarely in competition with the strongest players out there — and we can never win if that's the case. Ad formats, planning, execution, and technology need to be considered as a whole and not architected in fragmented pieces. Build with true customer journeys in mind.

02 — Loyalty is customer-centric, not data-centered.

Maintain the integrity of loyalty. Loyalty as a gateway to 'more customer data' is a disservice to our customers. Build loyalty programs in conjunction with retail media — with advertiser investments serving to enhance our customer's experiences.

03 — Own a direct relationship with advertisers.

Somewhere along the way we were convinced to cede our audience data and advertiser relationships to someone else to sell and manage. I'm not talking about partnering on the work — we all need experienced help in this journey. I'm talking about giving your customer data to someone and saying, "just write me a cheque." In every other part of the retail business, retailers own a direct relationship with their suppliers — so too should they in retail media.

04 — Chase mutually beneficial value.

Retail media is so much more than ads on a page — it's about creating mutually beneficial value for our customers, our advertisers, and ourselves. A big part of why retail media can and should be the dominant form of media in the future is because of the inextricable link between advertiser and publisher: we have very similar and complementary goals.

Europe's leapfrog moment.

Europe built the foundation for Retail Media 3.0 — the most difficult piece first. With those philosophies and strategies, it's working backwards to rewrite the narrative around the true value of this thing.

Retail media has evolved so much over the past 15+ years, but the central value proposition has not changed. And I'm reminded of that every time I'm in the European market.

Remember why we are all here… because millions of people shop every day. You simply can't get that anywhere else.

Comment, share, like. And if you want to read more, subscribe to the Retail Media Leapfrog Series on LinkedIn.