Every retailer that has dabbled in this space has their own internal flywheel that articulates their retail media value proposition against the broader business strategy — how retail media serves to feed the goals of the retailer. Inevitably, we all try to make these flywheels seamlessly fit for our three most important constituents. And it goes something like this:

-

The RetailerImprove profitability, drive more traffic, capture fair share, create a competitive moat, increase media weight.

-

The SupplierDrive incremental growth, conquest competitors, secure space, understand how people shop the brand, control how dollars are spent at retail.

-

The CustomerProvide them with… more relevant advertising.

In this week's Retail Media Leapfrog Series — articles that serve to help merchants, operators, and retail marketers leapfrog incumbents leveraging learnings from real retail media architects — we talk about the three body problem in retail media.

Clearly we've spent a heck of a lot of time thinking about the business problems we're addressing from the lens of a retailer and its suppliers, but not as much on the problems we're solving for our customers. And if we want to keep this retail media thing growing, we're going to need to think about the customer a lot more.

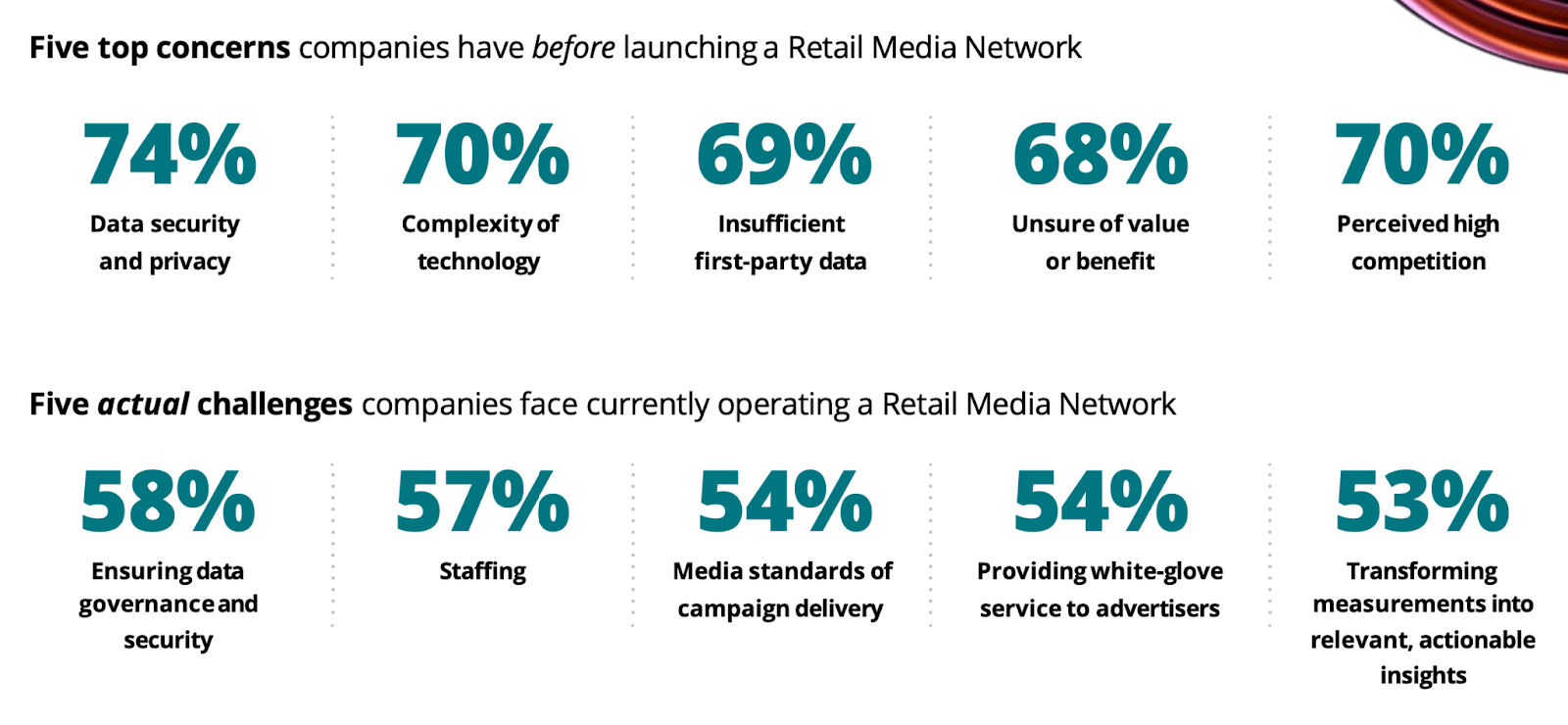

Body No. 01The retailer, by the numbers.

From a retailer perspective the benefits are clear, and where we spend our time is on the decision to build a retail media business, or the complexities of operating one. Deloitte Digital has great data on this from a 2023 survey of 450 retail executives in the U.S.

From data security to staffing to measurement, there's a lot to think about, because this is a relatively new business model for retailers. You'll notice the concerns make no reference to the two other bodies — the supplier and the customer.

Body No. 02The supplier, by the numbers.

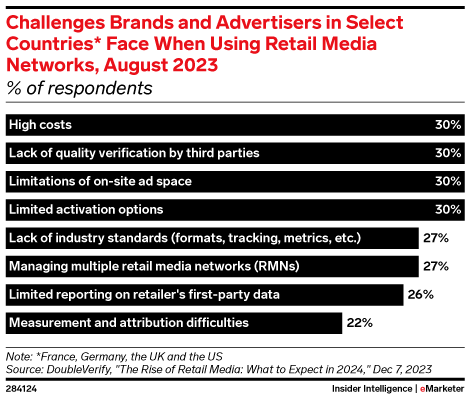

From a brand perspective, the focus is along the lines of: 'what is holding me back from investing at greater scale?'

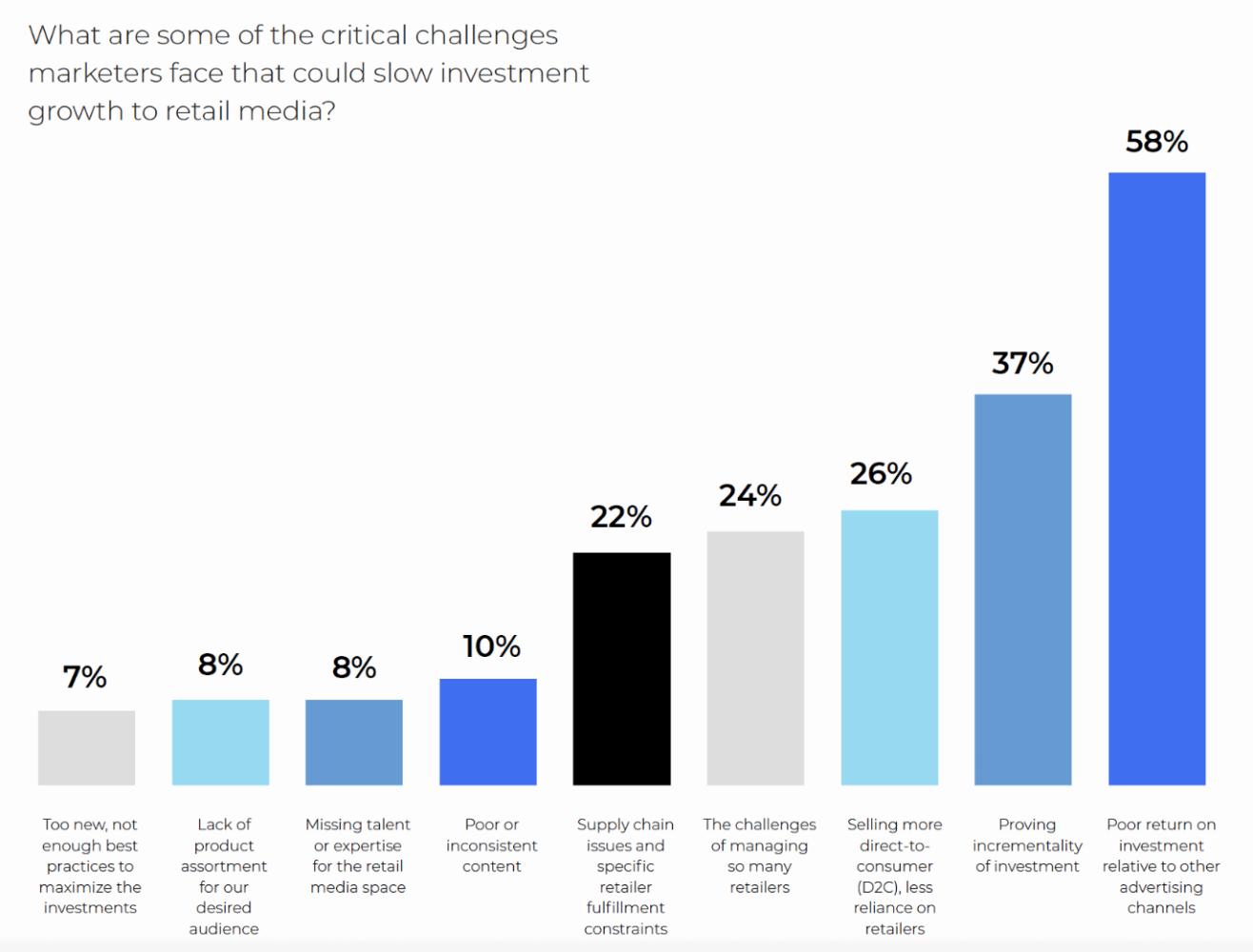

A 2023 DoubleVerify study suggests the core challenges brands face relate to cost, ad space, standardization, and measurement. These responses are pretty consistent across most surveys. Skai's 2023 study found additional challenges including supply chain and poor ROI.

Notice again that customer (shopper) considerations are not top-of-mind for brands either.

Body No. 03The customer, by the numbers.

One might argue the customer benefit isn't top-of-mind because it's obvious — 'of course it's good for them, they get more relevant ads!' But as a customer, when you get retargeted with the things you've already bought, or a system decides you fit a cohort for something else, does it make your shopping experience more joyful?

You could also argue that because it drives sales, it's clearly relevant, so they must like it. But that's a big leap — assuming that just because someone bought something off an ad, it was of value to their experience. So what is retail media's real value for the customer? Let's look at what that customer ultimately wants.

What does the customer want?

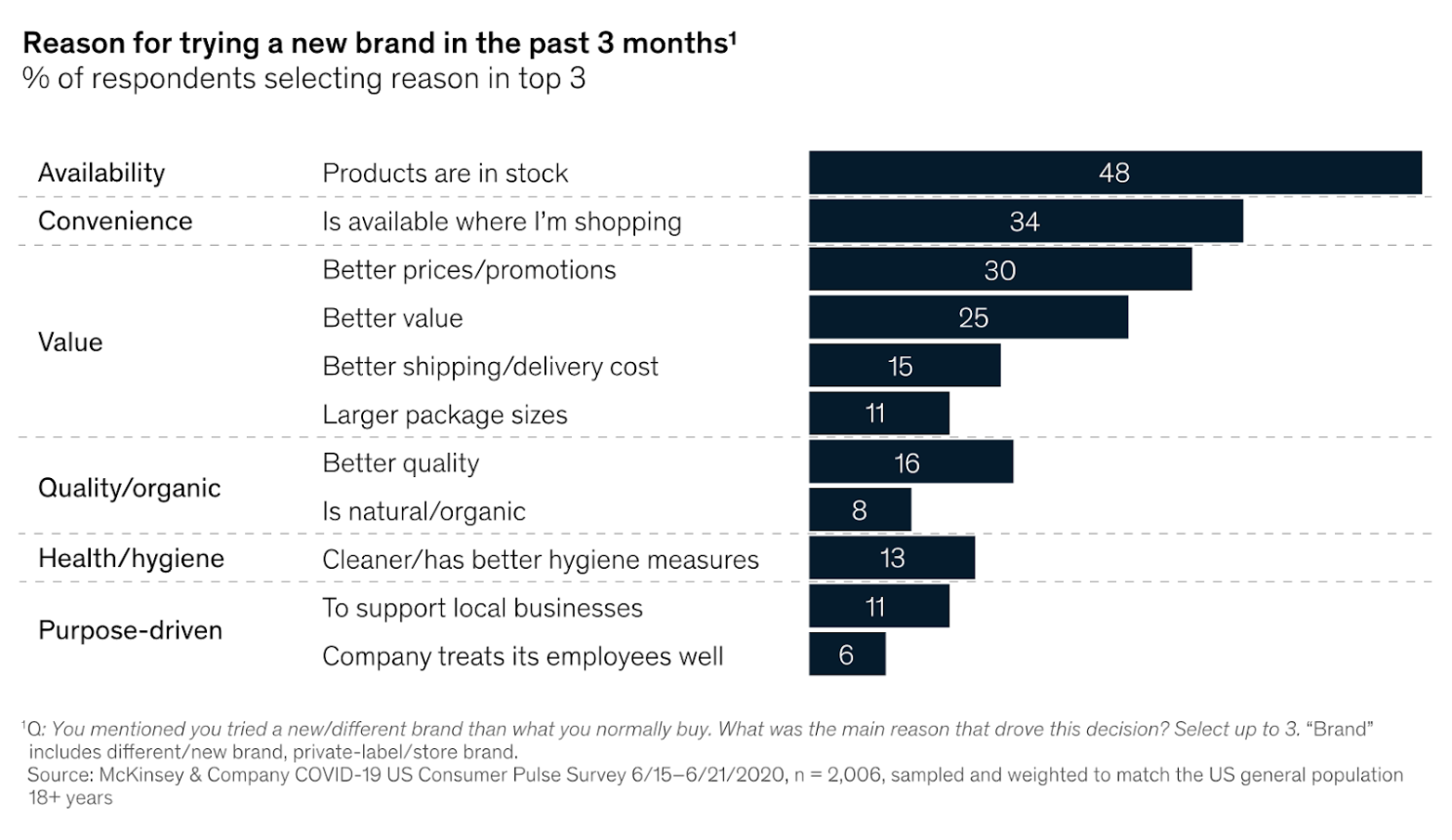

As it relates to 'buying something new,' a McKinsey & Company study found that product availability and value were by far the most important factors.

Many other surveys suggest that more information about the product is key to making a purchase decision — especially online. What customers want is reasonably consistent across the board:

- The thing I want to buy is available to purchase.

- It's the right value (pricing, quality).

- You make it easy for me to buy it — good information, easy-to-use tech, low shipping costs.

Does what we do in retail media support any of those things? Certainly — but indirectly.

How retail media indirectly impacts the customer.

Many of the early-stage retailers in the retail media space were grocers, operating on very thin margins (1–3%). Retail media can offer access to effective, high-margin dollars that can be reinvested in things like lower shipping costs for online grocery, easier-to-use platforms, or growth marketing — which can deliver economies of scale and ultimately reduce the cost of goods for consumers.

In this, retail media can tick at least two boxes of the 'customer wants' — it indirectly reduces the cost of goods, and it can reduce the cost of things like shipping. But what of the supplier in this equation? Are they not simply paying a premium to support better profitability at the retailer? Two considerations:

- There's an expected margin baked into media already — upwards of 50% — meaning that when brands advertise outside of retail, they're paying premiums for multiple intermediaries and the places those ads appear. It's how Facebook maintains a ~35% profit margin.

- Return on investment tied to retail media is relatively strong — meaning that, regardless of the premium cost of the ad, it's generating a positive return.

How retail media directly impacts the customer.

For this we turn to decades-old shopper marketing activations — events, in-store demos, at-home sampling and more. Co-funded activities that allow customers to experience products, be delighted, or have a little fun along their shopping journey.

Within the sphere of retail media, these activities are relatively new — having historically sat on separate teams within the retailer. And they're often slightly more complex to operate than programmatic ads, so they get a lot less attention.

But these more customer-centric, retail-media-powered activations work in spectacular ways — far beyond an ad in a retail search. For example, Sampler — who has powered omnichannel trial-based experiences for Kroger, Target, L'Oréal and more — ran a program with Starburst focused on increasing the quality of reviews on Target.com. By getting products into likely buyers' hands, they delighted potential buyers and increased the quality of reviews by 11.5%.

Solving the third body.

Retail media has the ability to offer so much more to our customers than just relevant ads. It can:

- Surprise and delight them.

- Create opportunities for trial.

- Build engaging experiences.

- Reduce the cost of shopping.

- Improve their shopping journey.

- Enhance content — and more.

As we think about how we continue to evolve this space for growth and longevity, we need to spend a lot more time focused on the benefits to our most important constituents. In this, we've solved the impossibly complex three body problem in retail media.

If this resonated, share it, comment, push back. And subscribe to the Retail Media Leapfrog Series for more.